European Sustainability Reporting Standards (ESRS) now approved!

On July 31st, the European Commission adopted the European Sustainability Reporting Standards (ESRS), i.e. the standards that should be used by companies subject to the CSRD (Corporate Sustainability Reporting Directive). Read about the standard here (or peruse the actual 245 page document here). The standards, despite having lost a little bit of edge and having been watered down during the final round of input/negotiations (read more here), are potentially ground breaking! They have the potential of changing not only accounting, but also how assets and activities are valued. By extension the standards will therefore also change business models. The changes promise to be massive. Only going through the ESRS and its disclosure requirements takes hours, if not days.

A key to understanding and working with the ESRS is the so-called “double materiality” (which refers to impact and financial materiality). According to the now adopted final version, more issues are subject to materiality; only once they are considered material does a company have to disclose them. From this follows, that though there are a number of general disclosure requirements the perhaps most important way of finding out what to report, is through the materiality analysis.

Personally, I welcome that move. I think it is important that companies focus on what is material as it strengthens their buy-in by saving time and reducing unnecessary frustration and resistance. I do see the risk with leaving the assessment of what is material to companies, but I believe that is a risk worth taking. And, besides, auditors will work on this element and practice will evolve.

Though I have written about CSRD and ESRS before (see previous Newsletters), and I have helped companies assess what they are expected to do, it is still unclear to me how certain features of the standards will turn out in practice. My hope – and expectation – is that the vast majority of companies reporting according to ESRS, will approach this with curiosity and a wish to improve the reporting landscape together. I think we have reached far enough for companies to be competent enough to assess risks and opportunities relating to sustainability, and to be transparent with the risks they are facing (imagine a tourism operator in Southern Europe not accounting for the risks associated with heat and wild fires). We are in this together, and it is together that we will build corporate culture and procedures that will contribute to a better planet for people and nature.

The European Union is now one of the main actors when it comes to pushing reporting requirements, but change is happening in many parts of the world. For a brief summary of the landscape regarding sustainability reporting in different parts of the world (the US, China, India, Canada and more), this article from Sri Lanka may be interesting. As the European Council and the Parliament has already approved CSRD no further approval is needed. However, within 2 month of adoption the Council or the Parliament may still object to the ESRS. However, time is now short for companies who will start using the Standards from January 1, 2024.

(don’t hesitate to contact We-ness if you need help with for example your double materiality analysis!)

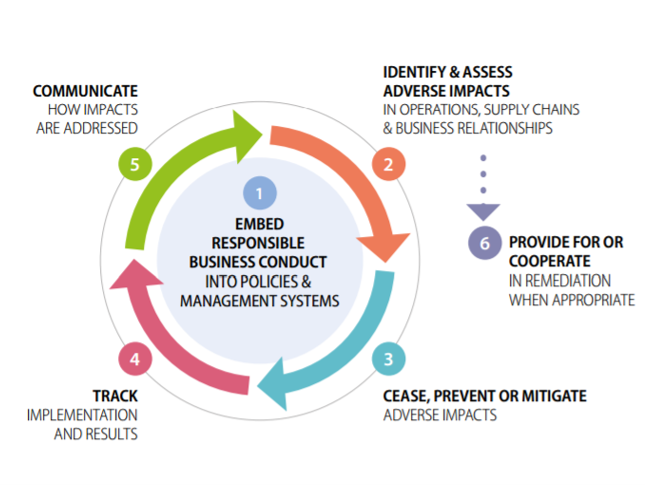

New OECD Guidelines for Responsible Business Conduct

In previous Newsletters, we discussed the upcoming legislation relating to due diligence of human rights and environment. A key document (which is also referred to in the Corporate Sustainability Due Diligence Directive relating to due diligence and responsible business conduct, is the OECD Guidelines for Multinational Enterprises on Responsible Business Conduct. The guidelines were recently updated and came into force in June.

The Guidelines are a little unique, as they are supported by an implementation mechanism consisting of National Contact Points appointed by national governments. Though I don’t think that the guidelines have changed substantially, some wording and some recommendations have been made stronger. The update did not include changes to the six-step due diligence framework (see below), which is now widely acknowledged as a template that companies can use when doing their sustainability due diligence.

Where are we at now, with regard to Agenda 2030?

July is estimated to have been the warmest recorded ever and human activities are to be blamed (read more). But the challenges are not only limited to climate; the recent high-level meeting in New York around the Sustainable Development Goals concluded that we have not yet managed to catch up the losses suffered during the COVID-19 pandemic. We were making good progress and many of us felt that the goals, including eradicating extreme poverty, would be a goal within reach.

It finds that many of the SDGs are moderately to severely off track (-report from the UN Secretary General, 2023)

Business as usual simply doesn’t seem to be good enough. Successful implementation of the 2030 Agenda for Sustainable Development needs to be a continued priority for governments, corporations, and civil society. There’s no reason – no point – in giving up.

Social Return on Investment

I have for a while sensed a growing interest in how businesses can – or should – reduce risks of doing harm and increase their positive contribution to society, and not only nature (which of course also is critical). Tools that try to account for the social value of activities, are sometimes able to include environmental aspects, at least indirectly (“non-financial impacts”).

In my experience managers (and a fair number of owners) from both public and private companies, are often interested in knowing what their impacts are, in addition to strictly financial returns. However, despite an increasing amount of data – which is largely thanks to regulations and voluntary reporting frameworks such as GRI (Global Reporting Initiative) and SASB (Sustainability Accounting Standards Board, from the US) – many decision makers still seem to struggle with what to measure, why and how. I personally believe it is a good idea to start with “why?” Is it to disclose information because of regulations, to learn and improve – or because of some other reason?

Depending on why you wish to measure, different options are available. The “tools” offered for working on social sustainability are many, and include Sustainability Return on Investment (S-ROI), Social Return on Investment (SROI), Total Cost Assessment (TCA) as well as more general instruments on measurement, such as Log Frame Analysis and Balanced Scorecards. The tools mentioned above are not necessarily mutually exclusive, and are often designed as instruments for management, rather than “only” measurement.

One of the most common approaches is the Social Return on Investment analysis, with its 7 (or 8) principles: 1. Involve stakeholders, 2. Understand what changes, 3. Value what matters, 4. Only include the material, 5. Don’t overclaim, 6. Be transparent, 7. Verify the results 8. Be responsive.

I have not found any single instrument that fits all needs, which is not surprising: the complexity of most workplaces normally requires some adaptation to specific needs.

For a more information on some of the pro’s and con’s with SROI this paper may be useful. I find that many companies who have not yet spent a lot of time quantifying their impact may be helped by making a distinction between focusing on externalities (meaning “by-product”) as opposed to an intended goal. In my view, it is now high time for companies to move from accounting for the value of sustainability, to managing for sustainability. Another way to look at it; we need to make use of all the data that is now available, to move from accounting to managing for results beyond finances. (this is part of stage 4 in a SROI-analysis, but my experience is that it ought to come in earlier, if we wish to use this as a management tool).

In the coming months, I will put additional effort into working on ways in which companies can become more sustainable with regard to their “social impact”. I intend to write about the progress but if you would wish your company to joint this process together with a handful of other companies, let me know!